Income tax freeze – what does it mean for taxpayers?

In last week’s Budget the Chancellor announced that the government will be freezing the income tax personal allowance and higher rate threshold between 2022 and 2026, rather than increasing them in line with inflation, which was the previous plan.

How much difference will this make? It depends on how high inflation is over the years in question. But the Office for Budget Responsibility (OBR) has made forecasts which allow us to make projections on this basis.

The personal allowance is the amount of income you can earn without paying any income tax on it. The higher rate threshold is the point at which the rate of tax you pay increases from 20 per cent to 40 per cent. (The situation for Scottish taxpayers is different – see below.)

The personal allowance this year (2020-21) is £12,500. It will increase in April 2021 as planned to £12,570, in line with inflation of 0.5% calculated according to the Consumer Prices Index (CPI). Similarly, the higher rate threshold will increase as planned from £50,000 to £50,270, again in line with CPI inflation.

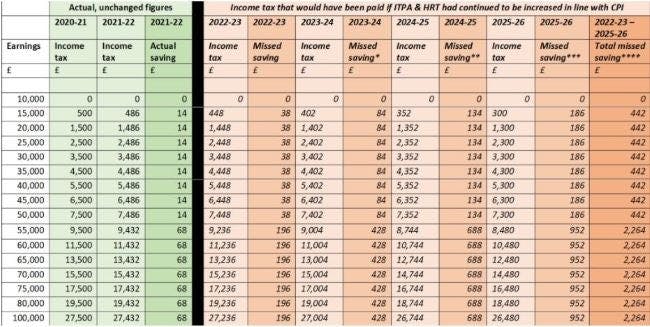

The table below shows, in the green shaded columns, the actual income tax that people earning the amounts in the far left column will pay in the 2020-21 and 2021-22 tax years, and the actual amount they will save in the 2021-22 year.

The columns in pink show the hypothetical income tax liabilities people would have if the income tax personal allowance (ITPA) and higher rate threshold (HRT) continued to be increased annually by CPI, and the saving that taxpayers will miss out on in that year because the ITPA and HRT will remain frozen at £12,570 and £50,270 respectively after 2021-22, until 2025-26.

This assumes CPI inflation of 1.5%, 1.8%, 1.9% and 1.9% when working out the increases to the ITPA and the HRT for the tax years 2022-23, 2023-24, 2024-25 and 2025-26 respectively, as per the OBR forecast in March 2021. It also assumes that the ITPA is rounded up to the nearest £10 and the HRT to the nearest £100. If they were increased by the forecast CPI inflation each year, on this basis we would expect in 2025-26 a Personal Allowance of £13,500 and a higher rate threshold of £54,100.

The final column adds up the missed savings for all four years 2022-23 to 2025-26.

It is important to note that these figures do not take account of National Insurance contributions (NIC). The government has confirmed that the NIC Upper Earnings Limit and Upper Profits Limit will continue to be tied to the income tax HRT. So, we know these thresholds will remain at £50,270 between 2022 and 2026. The Primary Threshold and Lower Profits Limit will continue to be set at fiscal events during this period, so they may continue to increase. If this were the case, since no NIC is paid on earnings/profits up to the Primary Threshold/Lower Profits Limit the band of earned income or profits on which the main NIC rates (12% on employment income and 9% on profits from self-employment) apply would decrease, thus reducing taxpayers’ NIC liabilities between 2022 and 2026. This is because the NIC rates drop from 12%/9% to 2% above the Upper Earnings Limit and Upper Profits Limit respectively. Note also that while employees do not pay NICs up to the Primary Threshold, they do have their rights to contributory benefits (including the state pension) protected by reference to a Lower Earnings Limit, whereby they are treated as paying notional NICs between this Lower Earnings Limit and the Primary Threshold.

The OBR estimate that this freeze in ITPA and HRT will, taking into account the freezing of the NIC Upper Earnings Limit and Upper Profits Limit too, raise an additional £1.555 billion for the Treasury in 2022-23, an additional £3.655 billion in 2023-24, an additional £5.79 billion in 2024-25 and an additional £8.18 billion in 2025-26.

Note that the table below applies to England, Wales and Northern Ireland. Scottish taxpayers pay Scottish income tax on their non-savings and non-dividend income. The freeze in the ITPA applies to Scottish taxpayers, but the freeze in the HRT only affects them insofar as they have savings and dividend income.

* The missed saving of £84 / £428 in 2022-23 is the missed saving from the predicted 1.5% CPI increase in ITPA / HRT in 2022-23 (£38 / £196) plus the missed saving from the predicted 1.8% CPI increase in ITPA / HRT in 2023-24 (£46 / £232).

** The missed saving of £134 / £688 in 2023-24 is the missed saving from the predicted 1.5% CPI increase in ITPA / HRT in 2022-23 (£38 / £196) plus the missed saving from the predicted 1.8% CPI increase in ITPA / HRT in 2023-24 (£46 / £232) plus the missed saving from the predicted 1.9% CPI increase in ITPA / HRT in 2024-25 (£50 / £260).

*** The missed saving of £186 / £952 in 2024-25 is the missed saving from the predicted 1.5% CPI increase in ITPA / HRT in 2022-23 (£38 / £196) plus the missed saving from the predicted 1.8% CPI increase in ITPA / HRT in 2023-24 (£46 / £232) plus the missed saving from the predicted 1.9% CPI increase in ITPA / HRT in 2024-25 (£50 / £260) plus the missed saving from the predicted 1.9% CPI increase in ITPA / HRT in 2025-26 (£52 / £264).

**** This is the total cumulative missed income tax saving over the four years, comparing the amount of income tax a taxpayer will pay with the freeze in ITPA and HRT to what they would have paid over the four years if ITPA and HRT had been increased in line with CPI inflation (based on OBR predictions).

Blog by Joanne Walker, CIOT Technical Officer