Deep dive: SEISS and Job Retention Scheme compared and contrasted

Guest blog by Tarlochan Lall, Barrister, CTA (Fellow), Monckton Chambers • The conditions for eligibility appear to be more stringent in comparison to the job retention scheme. The latest revisions expose anomalies in the provisions. • The framework for SEISS and its structure cast doubts over what entitlement it gives. HMRC’s message appears to be we’ll contact you, don’t contact us. • The lack of a dispute resolution mechanism creates issues for operators and HMRC alike. • HMRC’s guidance needs to be further refined as issues remain.

Individuals, self-employed as sole traders or partners who have been adversely affected due to coronavirus can claim a grant worth 80 per cent of their average monthly trading profit, up to a maximum of £2,500 a month. HMRC are contacting eligible individuals now and claims can be made from 13 May 2020. HMRC aims to make lump sum payments for the total grant up to a maximum of £7,500 from 25 May 2020.

It is estimated that approximately two million, of the circa five million self-employed in the UK, will not be covered by the SEISS (see the House of Commons Briefing Paper CBP 8879 updated at 28 April 2020 on the SEISS). Those excluded from the SEISS include the self-employed (a) whose income from self-employment is less than half of their total income; (b) who became self-employed after April 2019; (c) with annual self-employment income exceeding £50,000, subject to some anomalies; and (d) who are owner managers operating through companies. Exclusion (d) will cover the many freelancers who operate through companies, whether or not through choice. Freelancers operating through companies need to consider whether they can furlough themselves as owner managers and claim benefits under the Coronavirus Job Retention Scheme (“CJRS”).

Eligibility criteria for those not excluded from the scheme will disqualify many of the self-employed. A bigger issue is whether the potential claimant can establish eligibility; and the consequences of getting it wrong.

There is scope for disputes over ‘entitlement’ under the SEISS. However, there is no dispute resolution mechanism. Those not contacted by HMRC risk simply losing out without any legal recourse. It is emphasised that some form of dispute resolution mechanism is necessary because the SEISS provides for demarcation of those eligible and those not. The lock down has effect of adversely affecting businesses, large and small; and those businesses not compensated sufficiently would have legitimate grievances.

Comparison of the features of SEISS against those of the CJRS demonstrate a sharp contrast of the generosity of the CJRS against that of the SEISS; and the relative complexity of the SEISS. Most significantly, there is no express need to show the inability to pay workers under the CJRS, yet the self-employed will only qualify if they “have been adversely affected by reason of circumstances arising as a result of coronavirus or coronavirus disease” and “confirm to HMRC that [their] business has been adversely affected by coronavirus”. Business of any size can access the CJRS, yet eligibility criteria for the ‘micro’ self-employed appears to be more burdensome. That is in part, at least, due to state aid rules. SEISS is subject to the state aid rules essentially as it is selective, whereas the CJRS is not subject to state aid rules, essentially as it is not selective.

FRAMEWORK FOR SEISS

There are no express statutory provisions for the SEISS. The legal basis for SEISS is a combination of an enabling power in the Coronavirus Act 2020 (s76) and:

• HMRC’s core guidance first published on 27 March 2020 and updated on 14 and 21 April and 1 and 4 May 2020 (“core guidance”). That core guidance is supplemented by further guidance on:

o working out trading profits and non-trading income issued on 14 April and updated on 1 May 2020 (the “profits guidance”);

o how different circumstances affect SEISS issued on 1 May 2020 (the “further guidance”); and

• A Treasury Direction made on 30 April 2020 (the “SEISS Direction”).

A basic legal issue arising is whether the self-employed have any rights under SEISS despite the potential devastation caused to businesses by government action, albeit for good health reasons.

Essentially very similar legal issues arise in connection with the CJRS covered in my note of 16 April on the CJRS (see https://www.tax.org.uk/media-centre/blog/media-and-politics/%E2%80%98furlough%E2%80%99-coronavirus-job-retention-scheme-features-and-legal).

By way of summary, and in contrast to the CJRS:

• Although strong arguments can be made that the CJRS creates legitimate expectations, and therefore gives enforceable rights, there is greater doubt under the SEISS, principally owing to its terms (see below) and overall structure. My description of the CJRS is that it provides for pay and check later. In the case of SEISS, HMRC appears to have the power to initiate who can claim grants as they will ‘invite those eligible to make claims’. The message from HMRC appears to be we will contact you; don’t contact us. The SEISS Direction refers to “entitlement”, but doubts remain.

• The only avenue for any legal recourse would be judicial review, but that is likely to be extremely difficult to pursue successfully. Time being of the essence, as operators need help now, there is practical significance to these issues. A dispute resolution mechanism is expected to be introduced in the Finance Bill, but there is no time line for that yet.

• A dispute resolution mechanism is equally important for HMRC. For example, where a grant is paid but it transpires that there was no eligibility, it is necessary to establish what enforcement action HMRC can take and whether the grant can be clawed back.

• The SEISS Direction, like the Treasury Direction for CJRS, contains an anti-abuse provision. Similar issues as those for CJRS would arise but modified by specific conditions for SEISS in the guidance and the SEISS Direction.

It is understandable that owing to the emergency, policy announcements facilitate emergency measures. The policy announcements are expected to be put on a statutory footing with provisions in the Finance Bill. However, it remains to be seen which of the issues will be dealt with.

ELIGIBILITY

SEISS is for self-employed individuals and individual members of partnerships. There is no mention in any of the guidance of members of limited liability partnerships, which are bodies corporate, but treated as partnerships for tax purposes. Salaried members of LLPs can be furloughed under the CJRS as they are designated as employees for tax purposes. Consistency in approach would suggest that the tax treatment of LLPs determines eligibility and that non-salaried members of LLP should be treated as members of a partnership for SEISS purposes.

The conditions for eligibility specified are that the self-employed claimant (“S”) must:

1. carry on a trade the business of which has been affected by reason of circumstances arising as a result of coronavirus or coronavirus disease;

2. have submitted the self-assessment return for a relevant tax year. If that had not been done by 31 January 2020, an extension was granted to 23 April 2020. Failure to meet the extended deadline is a disqualifying event. By contrast, there is no direct requirement of compliance with, for example, PAYE filings under the CJRS;

3. have carried on a trade (which need not be the same trade) in both tax years 2018/19 and 2019/20;

4. intend to continue to trade in the period 6 April 2020 to 5 April 2021. Again, by contrast, there is no requirement under the CJRS for an employer to confirm that they will continue to employ furloughed employees;

5. meet the profits condition, namely “condition A, B or C” where S is not subject to the loan charge. Construction of the SEISS Direction indicates that meeting one of those conditions is sufficient. That construction is supported by the core guidance, which states that first the position for 2018/19 must be tested; and if eligibility is not established, HMRC look to 2016/17 and 2017/18 as well. Each condition as two limbs.

o The first limb of:

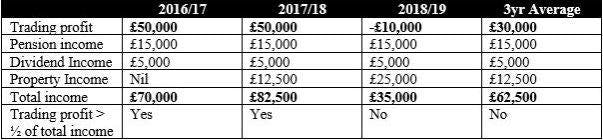

- Condition A is that in 2018/19, S must have trading profits between £1 and £50,000. S would fail condition A if profits exceed that limit or S has a loss in that year. However, it appears that provided the profits in that year are below £50,000, S would not be disqualified if the averaged profits over 2016/17 to 2018/2019 exceed £50,000. For example, if profits for each of those years were £99k, £62k and £49k respectively, giving an average of £70k over the three years, condition A would still be met, establishing eligibility. On this analysis, the outcome appears to be anomalous and inconsistent with the averaging described below. Another apparent anomaly is that if S carried on a trade in 2018/19, but had profits above £50,000, thereby failing condition A; did not trade in 2017/18, but did trade in 2016/17 with a profit below £50,000 or a loss giving an average of below £50,000, S would not be eligible because none of the conditions cater for this scenario;

- Condition B applies if S carried on trade in 2016/2017 to 2018/2019, when S must have average profits of between £1 and £50,000. An average loss over the three years disqualifies S. If condition A has been met, it appears that condition B does not need to be tested;

- Condition C applies if S traded in 2017/18 and 2018/2019 when S must have average profits of between £1 and £50,000. An average loss over the two years disqualifies S. Once again, if condition A has been met, it appears that condition C does not need to be tested.

o The second limb of each condition is that the trading profits so determined must be more than half of total income in:

- the tax year 2018/19, in the case of condition A;

- the tax years 2016/2017 to 2018/2019 in the case of condition B, and averaged; and

- the tax years 2017/18 and 2018/2019 in the case of condition C, again averaged.

o Non-residents who claim the remittance basis must certify that their trading profits are at least equal to their worldwide income.

- Where S is subject to the loan charge, S must satisfy condition D or E. Condition D applies if S carried on a trade in 2016/17 and 2017/2018 and had average profits between £1 and £50,000 for those years and also met the second limb of condition D for those years. Condition E applies if S did not trade in 2016/17 and had profits in the 2017/18 year between £1 and £50,000, again subject to meeting the second limb of condition E for 2017/18. 2018/2019 figures are ignored for the profit condition as those subject to the loan charge have until 30 September 2020 to file their 2018/19 return, although the 2018/2019 figures are ignored even if they have filed their return for that period. In such a case S must still meet the conditions of carrying on a trade which has been adversely affected and intend to continue to carry on a trade in the current 2020/21 year. Strictly it appears that disregard of the 2018/19 figures means that if S actually had profits above £50,000 for that year or had profits which would take relevant average profits above £50,000, S is not disqualified. Again, if this is correct, this also appears to be anomalous and inconsistent with the averaging provisions described, and even more advantageous than condition A.

Although filing of the 2018/19 SA return is an absolute requirement, it could have been spelt out that is also the case for the returns for 2016/17 and 2017/18. The SEISS Direction requires “a tax return for a relevant tax year” to have been delivered; and a relevant year is “all or any of the tax years” 2016/17 to 2018/19 for which trading profits and relevant income must be determined. The net effect is that tax returns for each of those years must have been delivered, although individual circumstances may give rise to specific issues. The profits guidance states that HMRC will use data on the tax returns submitted before 23 April 2020 although it had not been made clear that the 23 April 2020 deadline also applied to late 2016/17 and 2017/18 returns for eligibility under SEISS. The profits guidance also makes clear that late 2016/17 and 2017/18 SA returns submitted after 23 April 2020 will not be taken into account. It is also said that late 2018/19 returns will be “subject to additional anti-fraud checks”.

THE KEY ‘CONDITIONS’

Trading requirements

Three separate conditions require the claimant to have been trading in the last tax year, at the time of the claim (which is now implicit in the SEISS Direction provision that the purpose of SEISS is to provide for payments to be made to persons “carrying on a trade the business of which has been adversely affected…”) and having the intention to continue trading in the current tax year. Trade is defined in the SEISS Direction by reference to existing statutory definitions, but in practice, issues over the application of that definition may still arise.

Where a tax return for 2018/2019 has been filed declaring trading profits for that period, the condition for trading in that period should be satisfied, at least at first sight. Continuing the same activity into the current tax year should allow the other two conditions to be satisfied as the claimant should be able to show that it was trading, by virtue of carrying on the same activity, but for coronavirus. And provided there is no indication that the activity will not be continued after the lock down is lifted, the intention to continue trading should be met. Claimants are allowed to continue working during the lock down, so evidence of continuing work would assist claimants. Nevertheless, it remains to be seen whether HMRC will accept the subjective intention to continue trade, or also require some objective evidence to support the subjective intention, especially where businesses have no realistic hope of survival after the lockdown ends.

Those three conditions rest on a question of fact. Where questions arise whether or not there is a trade being carried on, HMRC normally adopt an investigative approach, which involves a detailed enquiry into the activities of the operator, which can be difficult and involves multifactorial assessment. Issues may arise in particular for relatively new ventures, especially if they have not been particularly profitable in early years and the operator has perhaps broken even or made a loss. Such operators would face issues over how much they can claim (see below) and the risk of being found not to be eligible for payments.

The guidance does not require that the same trade be carried on, as is the case for a number of tax reliefs. It is understood that a change of trade would not affect eligibility. Although the guidance does not specify the exclusion of any trades, it is also understood that property letting and furnished holiday lettings will not qualify.

Adverse impact of coronavirus

A requirement in the pre-1 May core guidance that eligibility turned on loss of profits has been dropped, possibly because all claimants would have had difficulty in demonstrating lost profitability, especially early in the tax year. The revised condition in the SEISS Direction that S’s business must have been adversely affected by coronavirus still does not have any materiality qualification. For example, it is not clear whether any financial adverse impact has to be shown. Examples in the core guidance refer to being unable to work, or having to scale down or temporarily stop, which indicate a low hurdle with no financial content for measuring adverse impact. That will benefit operators so long as that approach is adopted.

As payments will be based on previous years’ profits, and there is no condition quantifying adverse impact, some claimants may be financially better off. A claimant may only see a small or no reduction in profits or turnover but could still be eligible for the full grant (see the House of Commons Briefing Paper CBP 8879 of 8 April 2020 on the SEISS). Where, for example, work has been done or contracted for, but payment has not been received; or work has been started, put on hold and is expected to recommence, yielding the same income as if the lock down had not occurred, there may be no loss of profits. An operator who uses time during the lockdown to generate further work may even increase profitability in the current tax year.

By contrast, Denmark’s equivalent scheme given state aid approval, for example, firstly measures loss of turnover in March, April and May 2020 against average monthly turnover in 2019. Eligibility turns on decline in turnover of 30 per cent. The grant awarded is 75 per cent of lost turnover up to a maximum of €3,000 per month. No scheme designed at short notice is likely to achieve perfection. Even a turnover test gives rise to issue of its measurement. Continuing with the example above, it is not clear that where a contract has been secured, or work on contracts has been started and put on hold, would show a fall in turnover unless it can be shown that payments would have been received in March to May. However, it appears that stopping work would affect turnover, giving rise to eligibility. Additionally, the test of a 30 per cent drop in turnover due to coronavirus and the grant being linked to the expected loss of turnover appears to be targeting actual loss of revenue at the time of the lock down. It is understood that the French scheme also measures loss of income in March 2020 against March 2019, which appears to look to turnover; and eligibility turns of loss of income of 50 per cent due to corona virus. In comparison, the modified SEISS appears to be more generous.

The purpose of the comparisons above is not assessing, from an economic point of view, which scheme is better or cost effective to the taxpayer, which are policy matters. The comments are aimed at the workability of the scheme in practice. An operator deciding whether or not it can claim under SEISS would appear to have greater doubts over whether the eligibility criteria is met. It appears that claimants will be inclined to confirm that their business has been adversely affected as that may appear to be obvious. HMRC guidance states that they will “as usual use a risk-based approach to compliance”. That may not be satisfactory for either HMRC or taxpayers. Taking the examples and anomalies identified above, it appears the anti-abuse rule in the SEISS Direction will either not apply or only be capable of being applied in the most egregious cases. It appears if claims are processed, taxpayers will not necessarily know whether eligibility is confirmed or may be challenged later. Nevertheless, when making a claim, claimants will have to consider these matters. HMRC will have to decide when it is appropriate to challenge eligibility.

Another purpose of those comments concerns the overall equity of the scheme, in comparison to the CJRS, and consequences of breaching one or more eligibility conditions. Under the CJRS, for example the inability to pay worker’s wages does not appear to be a precondition to entitlement to claim grants for furloughed employees. The requirement to confirm adverse impact is a pre-condition to eligibility. That contrast appears to indicate unequal treatment, especially as potential SEISS participants are likely to be in an economically weaker position. Even if the adverse impact is a low hurdle as described, other judgement calls that need to be made, which at least in principle makes SEISS more onerous. Claimants will need to watch the fine print on any declarations required as they would be relevant to the legal consequences of any breach of the terms of the SEISS.

INCOME AND PROFITS

Trading profits

The starting point is that figures in tax returns will be used for identifying trading turnover, allowable business expenses and capital expenditure for establishing taxable profits. Examples of allowable expenses are given in the guidance, and it is confirmed that deductible capital allowances also count.

There is a concession that brought forward trading losses from previous years will not be deducted in calculating trading profits; but the averaging provisions appear to negate the concession for losses incurred in the last three tax years. An example in the guidance shows that where profits for each of 2016/17 and 2017/18 were £60,000 and there was a loss of £30,000 for 2018/19, the total profit for the three years is £90,000, which gives an average of £30,000 over three years. The grant is 80 per cent of the average, divided by 12 to give a monthly figure. On that example, £2,000 would be payable for each of March, April and May 2020. That example indicates that actual profits and losses are taken for the last three tax years in working out the payment. A formula for calculating the SEISS amount in the SEISS Direction gives the same result if the £30,000 loss was for 2016/17 and the £60,000 profits were for 2017/18 and 2018/19. In that calculation, say there were pre-2016/17 accumulated losses of £50,000. The taxable profits/loss for 2016/17 remain at £60,000/-£30,000, rather than being reduced to £10,000 or the loss being increased, so that is where the concession bites.

The example above shows the effect of essentially there being no concession for carrying back losses. If the losses for 2018/19 were also to be ignored, the total profit for the three years would be £120,000, or £40,000 averaged over three years. The full monthly grant of £2,500 would be payable because 80 per cent of £40,000 is £32,000, which divided by 12 gives £2,667. It appears anomalous to treat brought forward and ‘carry back’ losses differently as neither would be attributable to coronavirus.

The same applies to same year losses where S carries on more than one trade. A formula for calculating trading profits in the SEISS Direction provides for the deduction of trading losses against the trading income component of total income for the purposes of SEISS. That is confirmed by examples given in the profits guidance.

The formula for calculating the SEISS payment also confirms that in the anomalous situation identified above where the average profits over three years are £70,000, the SEISS payment is limited to £2,500 per month, which is the control mechanism, rather than denying eligibility.

Total income

The guidance makes clear that total income consists of income from earnings, trading profits, property income, dividends, savings income, pension income and miscellaneous income (including social security income). The figures will be derived from those disclosed in filed tax returns for the purpose of HMRC determining eligibility and inviting claims. There is nothing in the guidance or the SEISS Direction that would prevent HMRC looking beyond the tax returns, in cases where other income is identifiable, but was not reported. Claimants will have to consider disclosure of previously unreported income to ensure that they do not breach the eligibility criteria. Once again, it will be necessary to look at the small print in connection with claims and declarations required.

It would have been more helpful to have further guidance on property income, especially as there have been recent changes on deductions that can be made, in particular for interest. As information will be taken from tax returns, property income means net property income after allowable deductions, including for deductible interest. Given the historic entitlement to deduct interest, many landlords may have accumulated losses from lettings. If the thrust of the guidance that actual income over the last three tax years is taken, presumably brought forward losses which would otherwise reduce the taxable property income would be ignored. HMRC should clarify the position.

The following example expands on HMRC’s example given in the guidance. This example assumes that in 2016/17, before interest deductions were restricted, the mortgage interest of £50,000 was covered by rent of an equal amount, say for two or three rental properties, giving net taxable property income of nil and ignoring other expenses. In 2018/17 and 2018/19, the actual property income is also nil or is a loss; but that taxable property income increases as interest deductions are progressively restricted, and if any brought forward losses are ignored. However, if the figures are taken from the tax returns, which would not ignore the brought forward property income losses, the property income for 2017/18 and 2018/19 would be lower than those profits shown below and would most likely affect the final outcome.

STATE AID CONDITION

The core guidance states that if a person is above the state aid limits, or operates a trade through a trust, they should not claim the grant. The further guidance gives some steer on the state aid limits. The further guidance firstly confirms that the SEISS is state aid granted under the European Commission’s Temporary Framework (“ECTF”) which makes provisions for approving schemes designed to respond to coronavirus. The further guidance refers to a maximum limit of €800,000 per undertaking (and lower limits of €120,000 and 100,00 for those in agricultural sectors), which applies to all state aid, such as loans, but it is understood, not to tax that is deferred. Most business should not be affected by that limit.

The ECTF also refers to a condition that the business must not have been in difficulty at 31 December 2019, but there is no mention of that in the core or further guidance. It is understood that is probably because the EC’s approval of the UK’s scheme for SMEs does not refer to it either. As business have to give confirmation, it is important for them to know that the not in difficulty condition at 31 December 2019 does not apply to SEISS, and that tax deferred does not have to be counted, so HMRC’s confirmation on that would be welcomed.

The core guidance states that if a grant is claimed, HMRC will treat that as confirmation that the claimant is below the state aid limits. Claimants still need to check.

CONCLUSION

In economic terms, many operators within the aim of the SEISS are not in a materially different position from furloughed employees. Autonomy of self-employment is traded for the loss of statutory rights given to employees. Although the SEISS is well intentioned and needs to have safeguards, the conditions for government help appear to be more stringent than those for CJRS, which can be utilised by those more economically secure. And a number of key conditions give rise to legal and practical issues for operators perhaps not best placed to deal with them under economic strains of the time.

Guest blog by Tarlochan Lall, Barrister, CTA (Fellow), Monckton Chambers